Purchasing OEE: Cost-effectiveness of the material

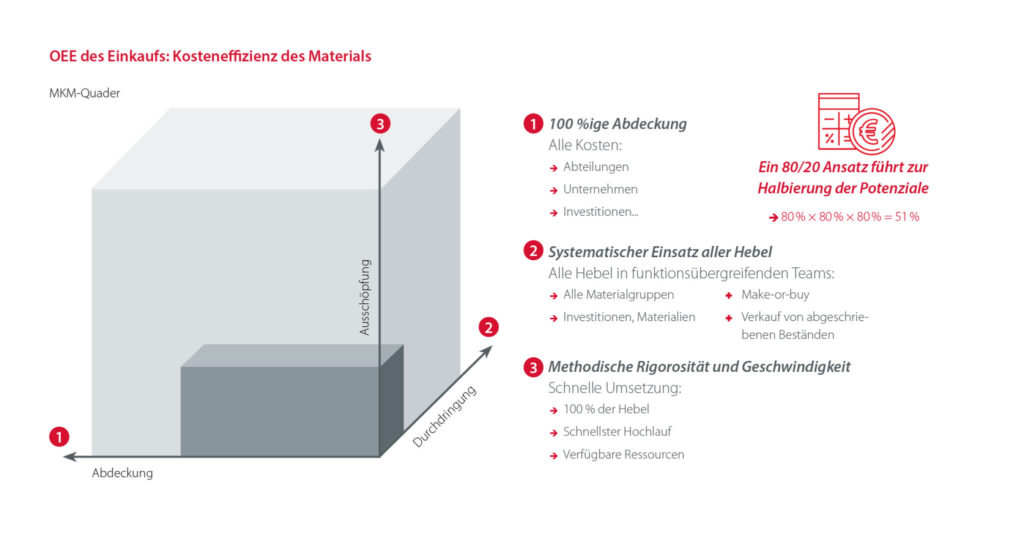

For the production manager, “Overall Equipment Effectiveness” (OEE) is a proven and reliable indicator for the objective measurement of performance in his area of responsibility. But what can the purchasing manager do to increase this? Initial offer minus negotiation result with permanently fluctuating prices? Costs of the last year minus costs of this year, with average rising commodity prices? What is the value of the C-parts whose production you would prefer to outsource? How can a purchasing manager show that every year he or she makes maximum progress with his or her company, masters sales markets, and implements sustainable cost strategies instead of dealing with short-term “price pressures”? And how can purchasing identify the need for action in order to create the necessary scope for achieving goals? The solution for a sustainable and continuous reduction of material costs is consistency and methodical rigorosity. This forces the MCM system. It also shows potentials and clarifies who needs to support purchasing in order to realize them. In order to reach the potential maximum, working in three dimensions is required:

- Cover plate: Recording of all plants, locations and material groups

- Penetration: Comprehensive processing of all purchased materials and services within each material group

- Exploitation: Methodical rigor in the identification and implementation of measures (use of all cost levers)

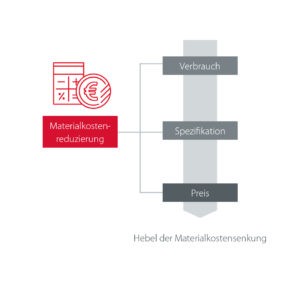

Material cost reduction lever

Project outcomes

- Depending on the industry, the savings achieved for direct materials typically range from 5% to 10%

- Savings in the indirect sector between 20% and 25%

- Ensuring your employees’ commitment to savings goals